See other National News Articles

Title: Dear Bureau Of Labor Statistics, Explain This 'Inflation' Anomaly...

Source:

[None]

URL Source: https://www.zerohedge.com/economics ... rs-housing-costs-soar-airfares

Published: Oct 13, 2021

Author: Tyler Durden

Post Date: 2021-10-13 14:26:21 by Horse

Keywords: None

Views: 80

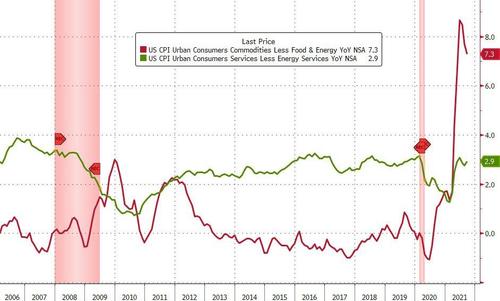

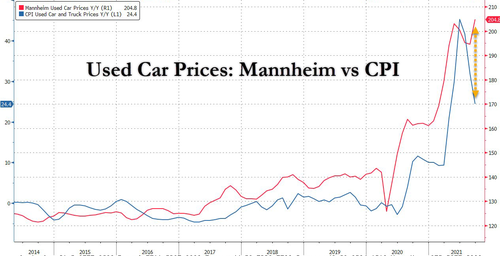

Having slowed for two straight months, whisper numbers predicted a slightly hotter than expected September CPI (edging up to 5.4% YoY, slightly above the consensus of 5.3%) on the back of a re-intensification of supply-chain bottlenecks due to a combination of natural disasters and COVID disruptions in the US and Asia kept pressure on manufactured goods in September. Headline CPI did indeed come hotter than expected (+0.4% MoM vs +0.3% exp) with the YoY spike edging back up to +5.4%...That is equal to its highest since July 2008. Source: Bloomberg Services prices rebounded while goods costs slowed their YoU growth very modestly (but remains at highest since 1981)... Source: Bloomberg Fuel Oil and Gas Utility prices dominated the MoM gains with Used Car prices actually dropping modestly (which is odd given that Manheim used car prices are at record highs)... Let us guess - hedonics? Or we would need a PhD to really understand? Core CPI's recent slowing picked up in September with a 0.2% MoM jump (vs +0.1% exp) leaving YoY flat around +4.0%.

Post Comment Private Reply Ignore Thread