See other National News Articles

Title: This Time Is Different The Fed's Next "Minsky Moment"

Source:

[None]

URL Source: https://www.zerohedge.com/markets/t ... ferent-feds-next-minsky-moment

Published: Feb 11, 2022

Author: Tyler Durden

Post Date: 2022-02-11 10:15:57 by Horse

Keywords: None

Views: 31

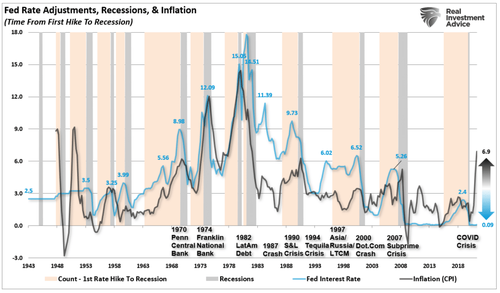

Authored by Lance Roberts via RealInvestmentAdvice.com, “This time is different.” Those are words usually uttered at the peak of bull markets throughout history for stock market investors. However, this time is likely different when it comes to the Fed and their current view of aggressively tightening monetary policy. To understand why “this time is different” for the Fed, we also need to know why the next “Minsky Moment” almost certainly awaits them. So, what exactly is a “Minskey Moment?” Economist Hyman Minsky argued that the economic cycle is driven more by surges in the banking system and credit supply than by the traditionally thought more critical relationship between companies and workers in the labor market. In other words, during periods of bullish speculation, if they last long enough, the excesses generated by reckless, speculative activity will eventually lead to a crisis. Of course, the longer the speculation occurs, the more severe the crisis. Hyman Minsky argued there is an inherent instability in financial markets. He postulated that an abnormally long bullish economic growth cycle would spur an asymmetric rise in market speculation, eventually resulting in market instability and collapse. A “Minsky Moment” crisis follows a prolonged period of bullish speculation, which is also associated with high amounts of debt taken on by both retail and institutional investors. One way to look at “leverage,” as it relates to the financial markets, is through “margin debt.” In periods of “high speculation,” investors are likely to be levered (borrow money) to invest, which leaves them with “negative” cash balances. This Time Is DIfferent Understanding what a “Minsky Moment” is makes it easier to understand why “this time is different” for the Fed as they approach their current monetary policy tightening cycle. Since 1980, every time the Fed tightened monetary policy by hiking rates, inflation remained “well contained.” The chart below shows the Fed funds rate compared to the consumer price index (CPI) as a proxy for inflation. There are three essential points in the chart above. The Fed tends to hike rates along with inflation, to the point it “breaks something” in the market. For the majority of the last 30-years the Fed has operated with inflation averaging well below 3%. The current spread between infaltion and the Fed funds rate is the largest on record. Historically, the Fed hiked rates to combat inflation by slowing economic growth. However, this time the Fed is hiking rates after short-term fiscal stimulus pulled-forward demand, creating inflationary pressures and a surge in wages. Combined with already high levels of leverage, an aggressive rate campaign is precisely the “catalyst” needed to ignite “instability.” The Fed Will Have To Choose In 2010, Ben Bernanke launched “quantitative easing” to lift asset prices, increasing consumer confidence. While that worked previously, it isn’t working now. More importantly, Jerome Powell and two other Fed members are heavily hinting at more aggressive policy. BOSTIC SAYS FED COULD EASILY PULL $1.5 TRILLION OF “EXCESS LIQUIDITY” FROM FINANCIAL SYSTEM. THEN WATCH MARKET REACTION FOR FURTHER BALANCE SHEET REDUCTIONS. MESTER: ABLE TO LET BAL SHEET TO RUN DOWN FASTER THAN LAST TIME. POWELL: WE EXPECT TO ALLOW BALANCE-SHEET RUNOFF LATER IN 2022. POWELL: BALANCE SHEET IS FAR ABOVE WHERE IT NEEDS TO BE. The problem with a more aggressive campaign, as Hyman Minsky alludes, is the potential unwinding of that leverage. Such has historically had poor outcomes. As noted above, the Fed didn’t have inflation during successive rounds of monetary interventions. The trillions in bond-buying programs did inflate asset prices, not to mention “wealth inequality.” However, Q.E. didn’t translate into surging price inflation. Such was because the Fed’s monetary interventions remained contained in the financial markets rather than leaking into the general economy. Today, however, is a very different story, and the Fed’s biggest problem is maintaining stability. The Fed’s ongoing interventions have created a “moral hazard” in the markets by inducing investors to believe they have an “insurance policy” against loss. Therefore, investors are willing to take on increasing levels of financial risk, as shown by yields of CCC-rated bonds. These are corporate bonds just one notch above “default” and should carry very high yields to compensate for that default risk. As noted, with the entirety of the financial ecosystem more heavily levered than ever, the “instability of stability” is now the most significant risk. The Fed must now choose between supporting asset prices and maintaining stability or combating inflation. It is a lose-lose proposition. Outcome Will Be The Same While the Fed is currently “hopeful” that economic growth will remain strong in 2022, they are likely to be very disappointed once again. Given the economic surge was a function of temporary liquidity, the expansion will also be just as transient. Savings rates and disposable incomes already show early signs of reversion. Unwittingly, the Fed has now become co-dependent on the markets. If they acknowledge the risk of weaker economic growth, the subsequent market sell-off would dampen consumer confidence and push economic growth rates lower. If they ignore inflation to keep asset prices elevated, inflation will eat into the consumer’s ability to sustain their standard of living. In turn, consumption will slow, and the economy will slide into a recession. The Fed has a tough challenge ahead of them with very few options. While increasing interest rates may not “initially” impact asset prices or the economy, it is a far different story to suggest that they won’t. There have been absolutely ZERO times in history the Federal Reserve began an interest-rate hiking campaign that did not eventually lead to a negative outcome. The Fed is now beginning to reduce accommodation at precisely the wrong time. Growing economic ambiguities in the U.S. and abroad: peak autos, peak housing, peak GDP. Excessive valuations that exceed earnings growth expectations. The failure of fiscal policy to ‘trickle down.’ Geopolitical risks Declining yield curves amid slowing economic growth. Record levels of private and public debt. Exceptionally low junk bond yields Such are the essential ingredients required for the next “Minsky Moment.” When will that be? We don’t know. What we do know is the Fed is going to make a “policy mistake” as “this time is different.” Unfortunately, the outcome won’t be. Poster Comment: Simpler saying: "A Minsky moment is when you sell the good stuff to pay for the bad stuff. Suppose you have a leveraged stock, your stock broker calls up to meet your new margin requirements, then you sell your gold and silver to pay for the stock that fell flat on its face.

Post Comment Private Reply Ignore Thread